If you are needing debt-payoff inspiration, Jina has some for you today! She and her husband, Chris, have worked hard, stayed focused and paid off a huge amount of debt!

So, go ahead Jina! Tell us everything!

Jina’s Story

Hi everyone! I’m Jina. I’m 35 years old, blogger at MyFinancialHill and Dental Hygienist, from Houston, TX. I live with my husband Chris and two rascal dogs.

I have to admit that I’ve made lots of financial mistakes in my 20’s and even up until my early 30’s. I never really learned how to manage my money. Whatever I made, I spent within the month. Whatever I couldn’t afford I just charged it on my credit cards or took out loans.

Over time, my husband Chris and I racked up $116,000 worth of debt not including our mortgage, it’s crazy I know. We finally got some sense knocked into us and took control of our finances.

Now, 21 months later, we have paid off $78,250 worth of debt and we are on track to be debt free (besides the mortgage) by the end of the year.

How much debt did you have to start with? How long did it take to pay off?

When my husband Chris and I sat down and tallied all our debt in September 2018, it was a whopping $116,000. I still can’t forget the feeling of how overwhelmed we felt. We weren’t sure if we’d ever make it out of debt. However, with the right tools and mindset we started kicking debt to the curb like it was nothing.

So far, it’s been 21 months and we have paid off $78,250. We made major initial progress when we first started the debt paying journey by knocking out $50,000 in the first 10 months of the process, which you can learn more about that here.

What triggered you to start your debt payoff process?

Prior to September 2018, when we first started our debt paying journey, we knew we had debt but we put it in the back of our minds.

I knew it was there but didn’t want to confront it. Maybe I didn’t want to face the reality of the situation. It was easier to ignore the debt and just keep living paycheck to paycheck, paying minimums along the way.

Before September of 2018, we were trying to pay down our debt by paying more than our minimums but it was not getting us anywhere because we never implemented any set strategies. Month after month, it felt like we were making no progress.

Then one day, Chris mentions how his co-worker followed Dave Ramsey’s debt paying principles and has a paid off mortgage. I was impressed and became curious about his methods.

We both sat down and started learning more about Dave Ramsey’s strategies like his infamous baby steps and snowball method. We became inspired from listening to other success stories and decided that we should try out his tools such as the Everydollar budgeting app and implement the snowball method to tackle our debt.

What was your debt consisted of?

We had a total of $116,000 which consisted of:

8 Credit Cards = $31,511

1 Car Loan = $2,439

2 Medical Loans = $3,500

My Student Loans = $38,904

Chris’ Student Loans = $18,819

1 Personal Loan Prosper = $10,827

1 Personal Loan From Family = $10,000

What was your income range throughout the debt free journey?

With both our incomes combined, it was around $120,000-$130,000 a year. Our incomes fluctuated depending on side hustles we did.

For Chris, he works in the office environment but for a short time he drove for UBER on the weekends and at nights to make extra money.

I usually worked 3 days but picked up extra shifts at other offices on my days off to make more money.

We both side hustled for a short time and ultimately decided to take it easy and not stress ourselves out too much.

Are there any specific things you did to help pay down debt?

The first thing we did before we started attacking debt was to make sure we had a hefty Emergency Fund in place.

We made sure we had at least 3-6 months worth of monthly expenses saved up before throwing every extra penny we had at debt. That gave us the peace of mind to be aggressive with attacking the debt because of the safety net we had in place.

We also started budgeting for the first time. It helped us track every single penny we had coming in and out of our accounts. I think that budgeting has been the most important aspect of this whole process. With the right budgeting tool, it really made it so simple to do.

We also looked for savings where we could find it.

Things we found cheaper rates for

- Electricity Bill

- Cell Phone (now we pay $80 flat for 2 lines unlimited talk, data, and text with Cricket Wireless, MetroPCS offers similar plans) *Note: here at Big House in the Woods, we use Red Pocket. You can check out that full review here.

- Home Owners Insurance

- Car Insurance

- Cable (Cheaper rates when switching providers when contract is up)

Other ways we saved

- Used cash back apps like Ibotta and Rakuten when I grocery shopped or purchased anything online

- Stopped buying lunch and dinner outside during the weekday, cooking mostly at home (we now limit buying restaurant food for the weekends as a treat)

- I had over $2,000 knocked off one of my Perkins Student Loans by filling out a form since I worked as a Dental Hygienist. (Other professions eligible, find out here)

- Minor home repairs done ourselves with a little research on YouTube. (I fixed my washer for under $18 with a YouTube video and purchasing an appliance part)

- Saved on grooming costs by washing one of my dogs at home. (The other one turns into a tasmanian devil when I try to groom him so he has to go to the groomers)

- Used our tax refund to pay down debt instead of going on a shopping spree

- We use credit card travel points for our trips and vacations.

- Saved on property taxes by filling out something called a “Property Tax Protest.”

Did you use any tools to help pay off debt? ex: apps, programs?

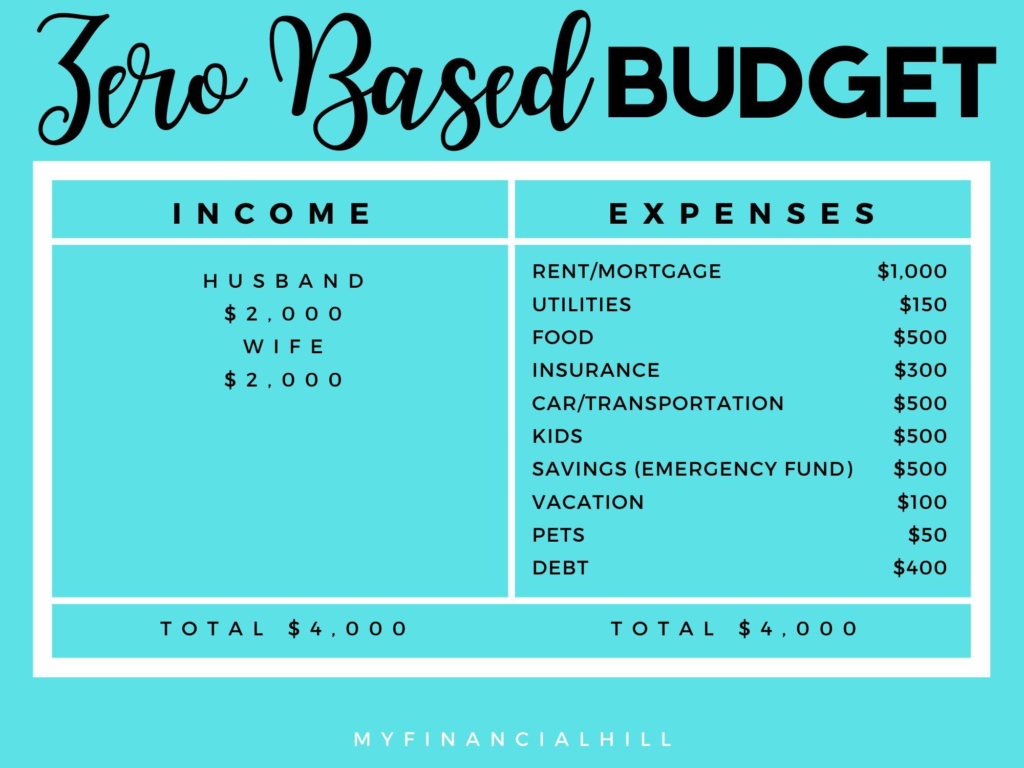

What helped us tremendously get control over our finances was budgeting! We used the Everydollar app (desktop/mobile app version available) which was free to use once you sign up.

With the Everydollar app, I was able to log in every single transaction for the month and keep track of all income and expenses which revealed our financial standing for the month.

Everydollar uses the zero-based budgeting method which is basically giving every dollar of your income a specific task to go towards an expense, saving, or debt category, leaving a zero balance.

Creating a budget gives you an outline and plan of how you will allocate your money every month. This has helped us tremendously with being able to come up with extra money to pay off our debt.

The way we use credit cards now is different. We use only 1 credit card for all our expenses and pay it off in full each month. Using a credit card also helps us to keep track of all expenses and makes it easier for us to log it into our monthly budget.

Did you use any debt payoff strategies? ex: snowball, avalanche, others?

We implemented The Snowball Method to pay off our debt which is to first list all our debts from descending order and start attacking debt with the smallest balances first. This method helped us knock out $50,000 within the first 10 months of the debt paying process.

Within this method, the focus is applied on the debts with the smallest balances while paying minimums on rest of the debt.

Basically, when the first debt item gets knocked out, you take the minimum for that first item and roll it over to the next item, which increases the payment applied for the second item. Keep going down the list until you finish paying off all debt.

By implementing this method, our “rollover money” grew to about $1,600 a month that we were able to use to apply towards our debt.

Here is a list of what we have paid off

8 Credit Cards = $31,511

1 Car Loan = $2,439

2 Medical Loans = $3,500

My Student Loans = $9,405

Chris’ Student Loans = $18,819

1 Personal Loan Prosper = $10,827

1 Personal Loan From Family = $1,749

Total = $78,250

All we have remaining is…

My Student Loan = $29,499

1 Personal Loan From Family = $8,251

Total = $37,750

What I liked about using the Snowball Method was the satisfaction we got from the many small victories when debt started getting eliminated one by one. This actually helped to motivate us as well.

How did you stay motivated throughout your debt free journey?

We stayed motivated by not fixating on how much we had to pay off. We just focused on one task at a time and slowly but surely we were making progress.

We would also listen to Debt Free Screams on Dave Ramsey’s Podcasts and that really helped with motivation.

I love hearing the success stories of others as it boosts hope and belief that achieving the debt free life is attainable.

How has your life changed from before and after paying off debt?

Prior to our debt free journey, we had no control over our finances. We lived impulsively and were irresponsible with our finances now that I think of it.

Whatever we wanted, we bought it right then and there using our credit cards. We ate out all the time because it was convenient. We had the mentality that it was okay to get anything we wanted just as long as we paid our minimums on the credit cards.

I am so glad we snapped out of it and finally took control of our life and money. Now, we’re more mindful of purchases because we don’t ever want to wind up where we were ever again.

The thing is, I can’t say that life feels so dramatically different from when we had enormous debt to where we are now.

With budgeting, we’re better able to plan for large purchases. We still allow ourselves to buy nice things here and there but we can afford it now since we prepare for it.

We create a budget item for the large purchases or vacations. That way we still get to enjoy our lives without depriving ourselves.

We’re still able to go on vacations and trips but we’re definitely more financially savvy about it by using credit card points and saving up for trips (COVID definitely put a damper on our vacations for this year).

We also reserve the weekends to order from restaurants so we can relax and enjoy the weekends.

I do have to say that going through paying off debt has changed my mentality. I look at things way differently now. I don’t care to drive the nicest car, go shopping every weekend, have the latest iphone, or buy fancy handbags.

Read: Why I Won’t Buy a Roomba, Keurig, Apple Watch, or Yeti Anything…even though I can afford them

I know that all these things have an impact on my financial future. That’s what I’m most focused about now.

Was there anything you wish you did differently during the debt free journey?

Actually, I don’t think I would change anything about this whole process. Once Chris and I made up our minds to get debt free, we took charge of our finances.

We did the best we could without sacrificing our happiness.

Sure, maybe Chris and I could work non stop to get out of debt faster but it’s important to remember that this journey is a marathon, not a sprint.

I believe that finding the right balance was essential in eventually finishing the debt payoff progress, we paid off $78,250 so far and we have $37,750 left to go at 21 months.

I’m hoping that we’ll be fully debt free by the end of this year.

How does it feel to be debt free or close to?

It feels amazing that we were able to pay off $78,250 so far in 21 months.

I was hoping to reach our debt payoff goal of $116,000 by September this year but COVID definitely put a wrench in our plans.

To pay off over $78,000 is still a huge accomplishment for us. I never thought it would be possible for us to get this far ahead. I honestly thought we would never get out of debt.

It just goes to show, with the right tools such as budgeting, debt payoff strategy, and mentality, anything is possible.

It feels great to know that we don’t have to pay a dime to credit card companies or other lenders besides our student loans and mortgage lender. Paying off consumer debt helps to keep more of our hard earned money in our pockets.

Now, we can focus more on paying off the rest of our debt, paying off the mortgage early, and investing in our financial future.

Would you like to offer any words of encouragement to other readers?

Don’t be afraid to confront your debt. That’s the only way you’ll be able to tackle it.

It can be scary to list all your debt and see the large number in front of you, but it’s just a number.

Your debt doesn’t define who you are and you can definitely change the outcome of your future.

Most importantly, you need to know what you’re working with so list all your debt, find the right budgeting plan that works for you, use the Snowball Method or Avalanche Method (pay debt with the highest interest rate first), and have faith in yourself.

Don’t fixate on the huge task ahead of you, take it one step at a time. The next thing you know, you will also be on your way to being debt free.

Also, a word from Edward Norton from Fight Club “We buy things we don’t need with money we don’t have to impress people we don’t like”. I came across this quote the other day and thought it was hilarious but so true!

Don’t let this quote be the story of your life!

Final Notes from Lindsey

Would you like to get started on a journey like Jina and Chris’? Start here.

I hope Jina’s story has inspired you!

All the best,

Lindsey

Like!! Great article post.Really thank you! Really Cool.

Thank you! I’m glad you enjoyed it!